Investment Weekly: Where are the anti-bubbles?

27 July 2026

Key takeaways

-

New UK Prime Minister Andy Burnham’s first week in the job has put UK public finances back in the spotlight. He has announced a “cost-of-living government” that aims to support households, alongside ambitions to invest more in infrastructure, housing and defence.

-

In an uncertain global environment characterised by fragmented geopolitics and less predictable rate cycles, investors are placing a higher premium on durable cash returns. Asian equities are becoming increasingly relevant in this context.

-

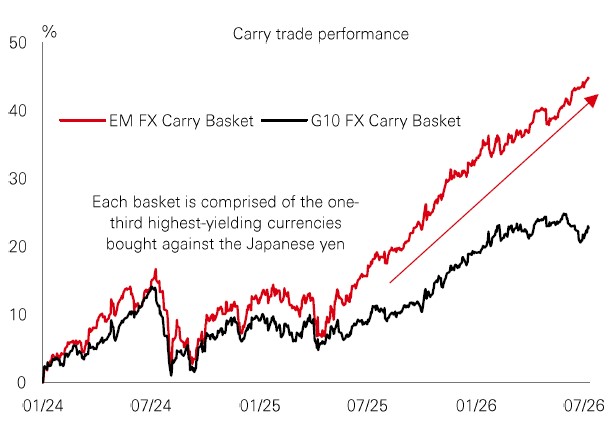

Carry trades — where investors borrow in a low-yielding currency to buy a high-yielding one —have performed exceptionally well over the past year, especially for EM FX. This has come amid persistently high EM policy rates and yields that have absorbed bouts of EM FX depreciation.

Chart of the week – Where are the anti-bubbles?

Many investors are worried about valuation bubbles. Depending on your perspective, these are either justified – based on supernormal profits and strong productivity – or a red flag for low future returns. But if you’re worried, what do you do? It’s a tougher question than usual because some traditional diversifiers have lost hedging power. Neither gold nor G7 bonds were reliable portfolio protectors during the market volatility in H1. There are three choices:

#1 Look beyond traditional bonds, but don’t abandon them. Many investors have been turning to “bond substitutes”, such as hedge funds. That makes sense – but there is still a case for G7 bonds too. After all, UK gilts outperformed the Magnificent Seven stocks in H1. But investors need to be careful; term premia are rising, and fiscal risks are top of mind. Shorter duration bonds could be a better way to take advantage of higher-for-longer rates.

#2 Income is back. There are income opportunities across emerging markets, credit and global stocks that can provide ballast to portfolios – even if they don’t hedge perfectly. Think real assets (like infrastructure), selective parts of private credit, or dividend-focused equity strategies.

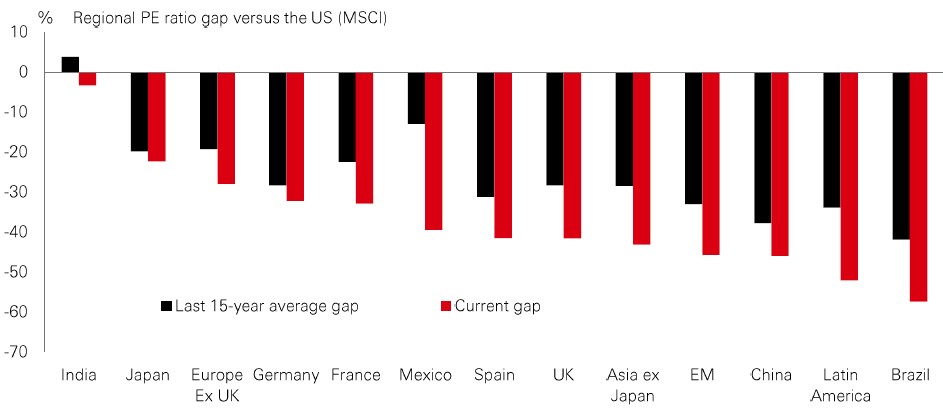

#3 Consider the “anti-bubbles”. These are parts of the market with the opposite characteristics of frothy bubbles: limited investor interest, relatively low valuations, and more sensitivity to potential rate cuts. By being less crowded – and more ignored – they may hold up better in a sell off. Examples include Europe and Asia, especially, China. This could be the most intriguing way to help protect a portfolio this summer.

Market Spotlight

Screen time

Using stock screens to filter out unwanted parts of an index is a common way of managing portfolios. In sustainable investment, it can be used to avoid climate risks, align portfolios to clients’ sustainability goals, and meet regulatory demands. One trade-off is that screening can cause portfolios to drift from the index – so it’s important to assess the impact on returns.

Small, focused exclusions – like stripping out coal producers – tend to leave returns and risk almost unchanged. But broad “zero tolerance” screens – for example, excluding oil & gas – can make portfolios behave meaningfully differently from the benchmark. That can cause noticeable relative under- or out-performance.

The impact of screens also depends on factors like the baseline year, market environment, and investment time horizon. For example, at the 10-year mark, the impact tends to be neutral or even positive. The direction of energy prices is also important, with EM indices more affected given their bigger weight in commodity names.

Overall, climate screens can be an important tool – but investors need to find a level of strictness that balances their objectives and tolerance for diverging from the benchmark.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. The level of yield is not guaranteed and may rise or fall in the future. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Source: HSBC Asset Management, Factset, Bloomberg, Macrobond. Data as at 7.30am UK time 24 July 2026.

Lens on…

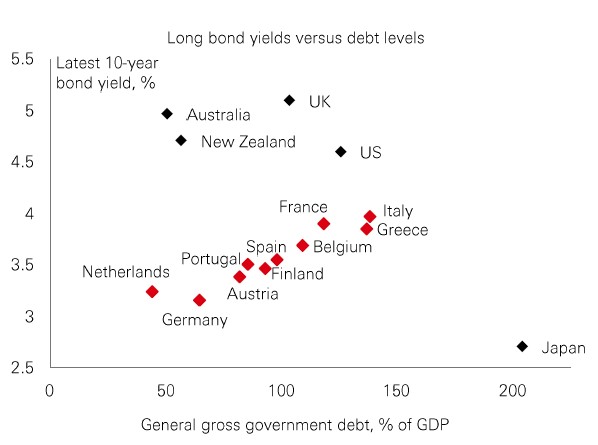

Burnham versus the bond market

New UK Prime Minister Andy Burnham’s first week in the job has put UK public finances back in the spotlight. He has announced a “cost-of-living government” that aims to support households, alongside ambitions to invest more in infrastructure, housing and defence. But he is up against a bond market that has been increasingly sensitive to any significant deviation from the government’s fiscal rules, which include reducing public debt as a share of GDP. The tug of war between governments and the bond market isn’t new, and isn’t specific to the UK. In many Western economies, the legacy of Covid and Russia’s invasion of Ukraine in 2022 has left public finances stretched, just as weak GDP and productivity growth have meant that tax revenues are struggling to keep up with spending priorities in the “multi-polar” world. These include boosting defence outlays as geopolitical threats rise, tackling climate change and energy security (with the closure of Hormuz sharpening policymakers’ attention), and addressing the cost of living amid rising anti-establishment sentiment. |

It is an environment where developed market bond yields are likely to remain high and more volatile than in the past.

Beyond growth

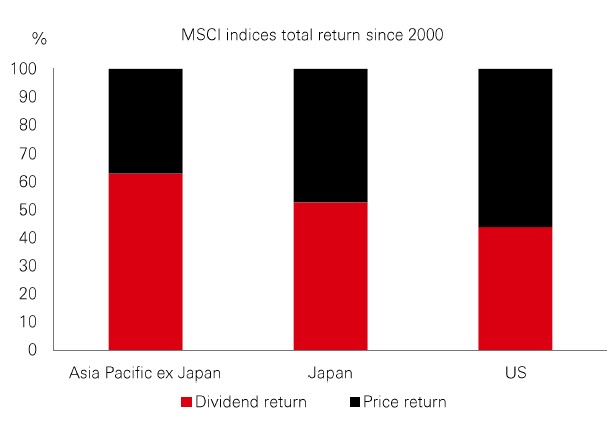

In an uncertain global environment characterised by fragmented geopolitics and less predictable rate cycles, investors are placing a higher premium on durable cash returns. Asian equities are becoming increasingly relevant in this context. Although often perceived as a play on the region’s stellar GDP growth, rising middle class and tech innovation, the reality is that income has been a significant driver of returns. Many Asian corporates hold stronger net cash positions than their Western peers, leaving room for high payout ratios, special dividends and buybacks as governance and capital-allocation discipline improve. Policy nudges matter too: South Korea’s Corporate Value-Up programme is encouraging clearer disclosure and stronger shareholder distribution, while measures in China promoting dividends and repurchases should support total returns. |

Active management remains central. The goal is not to maximise headline yield, but to scrutinise it — assessing leverage, free cash flow coverage and reinvestment needs, and diversifying across defensive, cyclical and growth names, while avoiding dividend traps built on fragile balance sheets.

Keep calm and carry on

Carry trades — where investors borrow in a low-yielding currency to buy a high-yielding one —have performed exceptionally well over the past year, especially for EM FX. This has come amid persistently high EM policy rates and yields that have absorbed bouts of EM FX depreciation. And for traders borrowing in yen to invest in EM assets, sustained yen depreciation has meant the underlying funding currency has become cheaper to repay, padding overall returns. But this is not just a story of yield gaps. A backdrop of low volatility in EM assets has reduced the risk of forced sales to cover losses. This points to a new regime of EM resilience in the face of external shocks – for example, dollar and commodity price volatility – that reflects stronger central bank credibility and improving fiscal fundamentals. |

Of course, there are risks to monitor. The yen could appreciate suddenly, or global volatility could spike if the AI trade wobbles. But for the time being, calmer markets and a cheap yen are likely to keep this trade in fashion.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Costs may vary with fluctuations in the exchange rate. Source: HSBC Asset Management. Macrobond, Bloomberg, Refinitiv, FactSet. Data as at 7.30am UK time 24 July 2026.

Key Events and Data Releases

Last week

This week ahead

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Source: HSBC Asset Management. Data as at 7.30am UK time 24 July 2026.

Market review

Persistent Middle East tensions lifted energy prices and core sovereign bond yields, weighing on sentiment. The US Treasury curve bear-flattened ahead of this week’s FOMC meeting as higher oil prices reinforced market expectations of Fed tightening. European yields also rose, as ECB President Lagarde signalled a near-term wait-and-see stance, citing potential second-round inflation effects. In equities, major US stock indices weakened on renewed doubts over AI investment returns as investors digested Q2 earnings from tech heavyweights, despite a rebound in the Philadelphia semiconductor index. European bourses edged lower, while the FTSE 100 moved higher. Asian stocks were mixed. The Nikkei 225 rebounded slightly, while the Kospi reversed gains, extending weekly losses. The Hang Seng and the Shanghai Composite rose, whereas the Sensex declined on rising trade concerns. In FX, the US dollar generally strengthened against major peers, with the JPY refreshing a multi-decade low.

Share

Related Insights

Disclaimer

This document or video is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document or video is distributed and/or made available by HSBC Bank (China) Company Limited, HSBC Bank (Singapore) Limited, HSBC Bank Middle East Limited (UAE), HSBC UK Bank Plc, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (20080100642 1 (807705-X)), HSBC Bank (Taiwan) Limited, HSBC Bank plc, Jersey Branch, HSBC Bank plc, Guernsey Branch, HSBC Bank plc in the Isle of Man, HSBC Continental Europe, Greece, The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank (Vietnam) Limited, PT Bank HSBC Indonesia (HBID), HSBC Bank (Uruguay) S.A. (HSBC Uruguay is authorised and oversought by Banco Central del Uruguay), The Hongkong and Shanghai Banking Corporation Limited – Philippine Branch, HSBC Investment and Insurance Brokerage, Philippines Inc, HSBC Insurance Brokerage Company Limited, HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group (collectively, the “Distributors”) and HSBC Bank Middle East Limited Qatar Branch, P.O. Box 57, Doha, Qatar (regulated by Qatar Central Bank for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority) to their respective clients. This document or video is for general circulation and information purposes only.

The contents of this document or video may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document or video must not be distributed in any jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document or video will be the responsibility of the user and may lead to legal proceedings. The material contained in this document or video is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document or video may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HBAP and the Distributors do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document or video has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed are based on the HSBC Global Investment Committee at the time of preparation and are subject to change at any time. These views may not necessarily indicate HSBC Asset Management‘s current portfolios’ composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients’ objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document or video is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investments are subject to market risks, read all investment related documents carefully.

This document or video provides a high-level overview of the recent economic environment and has been prepared for information purposes only. The views presented are those of HBAP and are based on HBAP’s global views and may not necessarily align with the Distributors’ local views. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. It is not intended to provide and should not be relied on for accounting, legal or tax advice. Before you make any investment decision, you may wish to consult an independent financial adviser. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether the investment product is suitable for you. You are advised to obtain appropriate professional advice where necessary.

The accuracy and/or completeness of any third-party information obtained from sources which we believe to be reliable might have not been independently verified, hence Customer must seek from several sources prior to making investment decision.

The following statement is only applicable to HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group with regard to how the publication is distributed to its customers: This publication is distributed by Wealth Insights of HSBC México, and its objective is for informational purposes only and should not be interpreted as an offer or invitation to buy or sell any security related to financial instruments, investments or other financial product. This communication is not intended to contain an exhaustive description of the considerations that may be important in making a decision to make any change and/or modification to any product, and what is contained or reflected in this report does not constitute, and is not intended to constitute, nor should it be construed as advice, investment advice or a recommendation, offer or solicitation to buy or sell any service, product, security, merchandise, currency or any other asset.

Receiving parties should not consider this document as a substitute for their own judgment. The past performance of the securities or financial instruments mentioned herein is not necessarily indicative of future results. All information, as well as prices indicated, are subject to change without prior notice; Wealth Insights of HSBC Mexico is not obliged to update or keep it current or to give any notification in the event that the information presented here undergoes any update or change. The securities and investment products described herein may not be suitable for sale in all jurisdictions or may not be suitable for some categories of investors.

The information contained in this communication is derived from a variety of sources deemed reliable; however, its accuracy or completeness cannot be guaranteed. HSBC México will not be responsible for any loss or damage of any kind that may arise from transmission errors, inaccuracies, omissions, changes in market factors or conditions, or any other circumstance beyond the control of HSBC. Different HSBC legal entities may carry out distribution of Wealth Insights internationally in accordance with local regulatory requirements.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/ business. However, the Bank disclaims any guarantee on the management or operation performance of the trust business.

The following statement is only applicable to PT Bank HSBC Indonesia (“HBID”): PT Bank HSBC Indonesia (“HBID”) is licensed and supervised by Indonesia Financial Services Authority (“OJK”). Customer must understand that historical performance does not guarantee future performance. Investment product that are offered in HBID is third party products, HBID is a selling agent for third party product such as Mutual Fund and Bonds. HBID and HSBC Group (HSBC Holdings Plc and its subsidiaries and associates company or any of its branches) does not guarantee the underlying investment, principal or return on customer investment. Investment in Mutual Funds and Bonds is not covered by the deposit insurance program of the Indonesian Deposit Insurance Corporation (LPS).

Important information on ESG and sustainable investing

Today we finance a number of industries that significantly contribute to greenhouse gas emissions. We have a strategy to help our customers to reduce their emissions and to reduce our own. For more information visit www.hsbc.com/sustainability.

In broad terms “ESG and sustainable investing” products include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors to varying degrees. Certain instruments we classify as sustainable may be in the process of changing to deliver sustainability outcomes. There is no guarantee that ESG and Sustainable investing products will produce returns similar to those which don’t consider these factors. ESG and Sustainable investing products may diverge from traditional market benchmarks. In addition, there is no standard definition of, or measurement criteria for, ESG and Sustainable investing or the impact of ESG and Sustainable investing products. ESG and Sustainable investing and related impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the ESG / sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of ESG / sustainability impact will be achieved. ESG and Sustainable investing is an evolving area and new regulations are being developed which will affect how investments can be categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.

THE CONTENTS OF THIS DOCUMENT OR VIDEO HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN HONG KONG OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT OR VIDEO. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT OR VIDEO, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

© Copyright 2026. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document or video may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.