13 Apr 2026

Geopolitical risk premiums compressed, and markets rallied last week after the news of the US/Iran ceasefire. But what should investors be watching now?

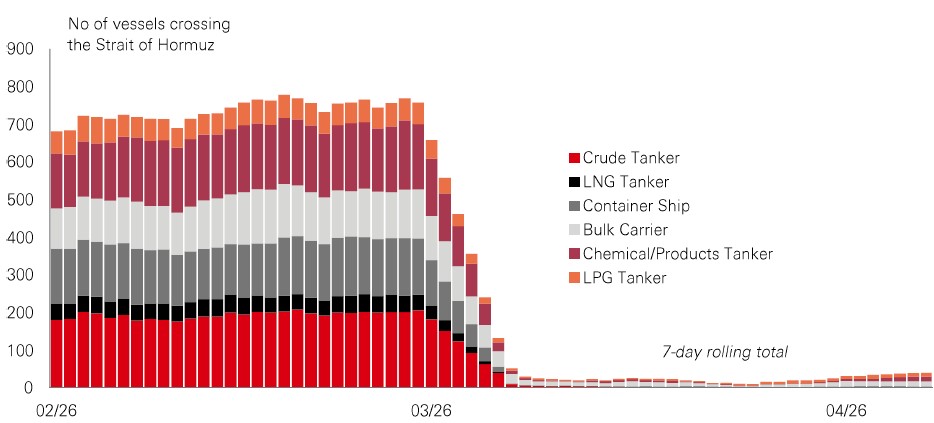

First, the key macro variable is how quickly vessel crossings at the Strait of Hormuz rise. The strait is a strategic chokepoint and a hinge factor for what happens next. If the data confirms a re-opening is underway and crossings are serially increasing, risk assets can continue to rally, even if other issues around the conflict remain unresolved.

Second, we look at the trend in oil prices. Brent and WTI prices have dropped back after a rapid rise, which even outpaced what we saw in the early part of the Ukraine crisis in 2022. But the spread between spot and futures prices remains elevated: around USD20 compared to 9-month ahead Brent. It takes around four days for oil tankers to reach India. If supply disruptions are progressively easing, the oil futures curve will flatten, supporting investor sentiment.

Third, it’s about policy interest rate expectations. In bond markets, traders have fretted that stagflation vibes would force rate-setters at the Bank of England and the European Central Bank to hike. Bets for Fed rate cuts later in 2026 were also taken off. But central bank watching is about both tracking the data and understanding the minds of policymakers. If the strait re-opens and oil futures curves drop, they will be more comfortable to “look through” the energy shock and not hike rates.

The stellar performance of “China Tech” was a major market theme last year. And while developments in the Middle East have recently shifted investor attention, China’s technology story continues to race ahead.

The country’s recent five-year plan stressed that tech capability remains a key priority, together with boosting productivity and economic self-reliance. This reflects efforts to rebalance the economy as a solid domestic growth engine. For investors, this focus on productivity-driven expansion is showing up in the performance of Chinese stocks.

Over the past two years, the Shenzhen Chinext index – the so-called “China Nasdaq” – has seen a remarkable double-digit return. While it’s more volatile than the US Nasdaq, Chinext has outperformed its counterpart, helped by heavy exposure to advanced manufacturing, green energy and semiconductors – all sectors that domestic policy is supporting. It comes as the broader Chinese market is seeing a switch from persistent downward profits revisions to a profits-driven recovery. While last year’s performance lifted valuations, they remain moderate relative to both longer-term averages and global peers. With tech, AI and other innovation-led industries central to the market outlook, China Tech looks set to remain a major theme.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Source: HSBC Asset Management, Bloomberg, Macrobond. Data as at 7.30am UK time 10 April 2026. Asset class performance is represented by different indices. US 60/40: Bloomberg EQ:FI 60:40 Index, 10yr UST: ICE BofA 10yr US Treasury Index, Global IG: Bloomberg Barclays Global IG Total Return Index unhedged. EMD local currency: JP Morgan EMBI Global Total Return local currency. Global Equities: MSCI ACWI Net Total Return USD Index. China: MSCI China Index, India: MSCI India Index. Frontier: MSCI Frontier Markets Total Return Index. Alternatives: USD: DXY Index, Gold Spot $/OZ, Infra Equity: Dow Jones Brookfields Global Infrastructure Total Return Index, REITS Real Estate: FTSE EPRA/NAREIT Global Index TR USD. **Crypto: Bloomberg Galaxy Crypto Index. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

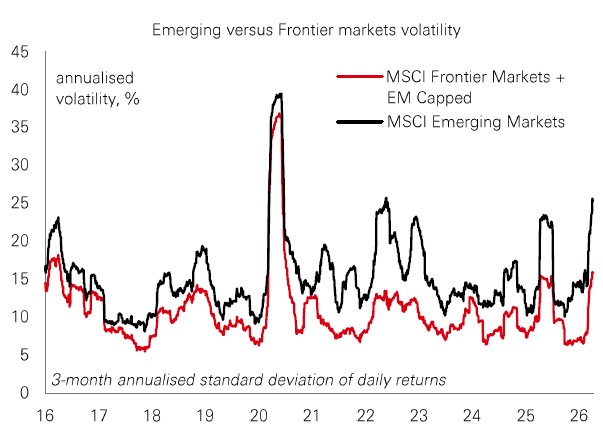

A lot has been said about the resilience of emerging market (EM) assets during the Iran conflict so far. That makes sense when you think about the fundamental changes built into emerging market economies over the past few years, whether in the form of improved fiscal and external balances, or enhanced policy frameworks. But what has also been quite impressive is the performance of frontier market stocks during this phase. The peak drawdown was limited to around 8%, versus 13% for EM. |

This highlights a long-standing theme when it comes to exposure to frontier market equities: they are usually less volatile. In this episode, the emerging markets index is exposed via its big weighting in Asian economies that depend heavily on gulf energy supplies, whereas key frontier markets (like Vietnam, Romania, and Kazakhstan) are less affected. Structurally, frontier markets are also insulated by a strong domestic ownership base that is less sensitive to global swings in risk appetite. A valuation discount versus EM peers also provides a natural downside buffer.

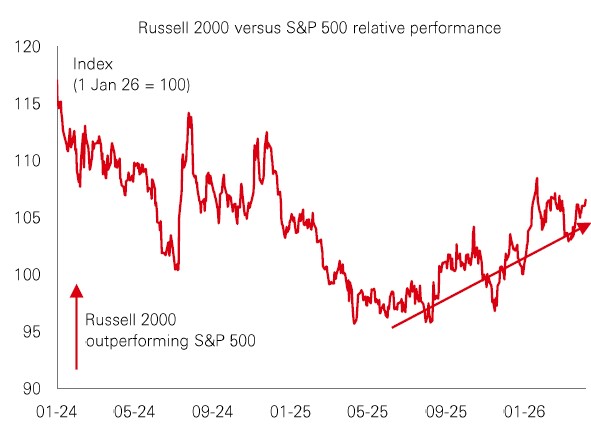

Since last summer, the trend has been for small caps to outperform large caps, helped by expectations of more rate cuts in 2026. So, when markets repriced in a much more hawkish direction last month, it would have been reasonable to assume that small caps would be pummelled. Rather, following an initial sell-off, there was a quick bounce back. We think this reflects two aspects of the broadening-out story. First, there are the “good” attributes of small caps in the current environment. Their big domestic revenue base is a virtue in a world of higher tariffs and energy prices that make global supply chains and logistics more expensive. In the US, the small-cap index has a significant weighting in energy firms, which remain big winners from the AI and broader capex buildout. |

Second, there are the “bad” vibes around the AI boom. Large-cap tech is now perceived to be capital-intensive with a lower ROI. The distribution of risks around future profits has widened, and the market is placing a premium on predictable cash flows. Overall, a mix of the “good” and the “bad” means that the broadening-out story can remain intact even in a higher-for-longer rate environment.

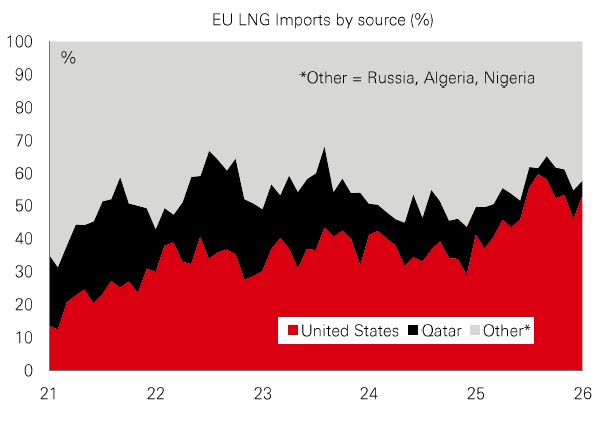

Last week’s sharp recovery in European stocks was unsurprising given the region’s dependency on imported energy supplies. But could Europe’s vulnerability have been overestimated in the first place? For starters, there has been a big push into renewables since 2022, including through REPowerEU. This has reduced dependence on gas and made electricity prices less mechanically tied to gas price spikes. Increased utility hedging has also dampened volatility. Europe’s LNG mix has also shifted, with most imports now coming from the US. And the EU has made storage targets more flexible versus 2022, especially under unfavourable conditions such as now, reducing the risk of a panicked buyer stampede and a further spike in prices. |

With the crisis less acute than it was in 2022, the overall government response to help shield consumers and businesses is also likely to be much weaker, especially with the bond vigilantes breathing down their necks. With growth more fragile than in 2022, the ECB will be under less pressure to offset the pickup in inflation. The recovery in the region’s risk assets could have further to go.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Costs may vary with fluctuations in the exchange rate. Source: HSBC Asset Management. Macrobond, Bloomberg, European Central Bank, Refinitiv. Data as at 7.30am UK time 10 April 2026.

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Source: HSBC Asset Management. Data as at 7.30am UK time 10 April 2026.

Global stocks rallied last week, as the US and Iran agreed to a two-week truce amid the ongoing Middle Eastern conflict. In developed markets, Japanese stocks led the gains. European and US indices also rallied on positive sentiment. In emerging markets, gains were broad-based, with large gains in South Korea and India. Government bonds ended a volatile week marginally higher, as sharp gains earlier in the week faded. Meanwhile, investment grade and high yield bonds strengthened. In FX, the US dollar ended lower while sterling and the euro appreciated. In oil markets, Brent crude prices were volatile but ended the week sharply lower, despite uncertainty over the credibility of the announced ceasefire. In precious metals, gold prices moved higher, reversing the previous week's declines.

This document or video is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document or video is distributed and/or made available, HSBC Bank (China) Company Limited, HSBC Bank (Singapore) Limited, HSBC Bank Middle East Limited (UAE), HSBC UK Bank Plc, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (20080100642 1 (807705-X)), HSBC Bank (Taiwan) Limited, HSBC Bank plc, Jersey Branch, HSBC Bank plc, Guernsey Branch, HSBC Bank plc in the Isle of Man, HSBC Continental Europe, Greece, The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank (Vietnam) Limited, PT Bank HSBC Indonesia (HBID), HSBC Bank (Uruguay) S.A. (HSBC Uruguay is authorised and oversought by Banco Central del Uruguay), HBAP Sri Lanka Branch, The Hongkong and Shanghai Banking Corporation Limited – Philippine Branch, HSBC Investment and Insurance Brokerage, Philippines Inc, and HSBC FinTech Services (Shanghai) Company Limited and HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group (collectively, the “Distributors”) to their respective clients. This document or video is for general circulation and information purposes only.

The contents of this document or video may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document or video must not be distributed in any jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document or video will be the responsibility of the user and may lead to legal proceedings. The material contained in this document or video is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document or video may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HBAP and the Distributors do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document or video has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed are based on the HSBC Global Investment Committee at the time of preparation and are subject to change at any time. These views may not necessarily indicate HSBC Asset Management‘s current portfolios’ composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients’ objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document or video is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investments are subject to market risks, read all investment related documents carefully.

This document or video provides a high-level overview of the recent economic environment and has been prepared for information purposes only. The views presented are those of HBAP and are based on HBAP’s global views and may not necessarily align with the Distributors’ local views. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. It is not intended to provide and should not be relied on for accounting, legal or tax advice. Before you make any investment decision, you may wish to consult an independent financial adviser. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether the investment product is suitable for you. You are advised to obtain appropriate professional advice where necessary.

The accuracy and/or completeness of any third-party information obtained from sources which we believe to be reliable might have not been independently verified, hence Customer must seek from several sources prior to making investment decision.

The following statement is only applicable to HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group with regard to how the publication is distributed to its customers: This publication is distributed by Wealth Insights of HSBC México, and its objective is for informational purposes only and should not be interpreted as an offer or invitation to buy or sell any security related to financial instruments, investments or other financial product. This communication is not intended to contain an exhaustive description of the considerations that may be important in making a decision to make any change and/or modification to any product, and what is contained or reflected in this report does not constitute, and is not intended to constitute, nor should it be construed as advice, investment advice or a recommendation, offer or solicitation to buy or sell any service, product, security, merchandise, currency or any other asset.

Receiving parties should not consider this document as a substitute for their own judgment. The past performance of the securities or financial instruments mentioned herein is not necessarily indicative of future results. All information, as well as prices indicated, are subject to change without prior notice; Wealth Insights of HSBC Mexico is not obliged to update or keep it current or to give any notification in the event that the information presented here undergoes any update or change. The securities and investment products described herein may not be suitable for sale in all jurisdictions or may not be suitable for some categories of investors.

The information contained in this communication is derived from a variety of sources deemed reliable; however, its accuracy or completeness cannot be guaranteed. HSBC México will not be responsible for any loss or damage of any kind that may arise from transmission errors, inaccuracies, omissions, changes in market factors or conditions, or any other circumstance beyond the control of HSBC. Different HSBC legal entities may carry out distribution of Wealth Insights internationally in accordance with local regulatory requirements.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/ business. However, the Bank disclaims any guarantee on the management or operation performance of the trust business.

The following statement is only applicable to PT Bank HSBC Indonesia (“HBID”): PT Bank HSBC Indonesia (“HBID”) is licensed and supervised by Indonesia Financial Services Authority (“OJK”). Customer must understand that historical performance does not guarantee future performance. Investment product that are offered in HBID is third party products, HBID is a selling agent for third party product such as Mutual Fund and Bonds. HBID and HSBC Group (HSBC Holdings Plc and its subsidiaries and associates company or any of its branches) does not guarantee the underlying investment, principal or return on customer investment. Investment in Mutual Funds and Bonds is not covered by the deposit insurance program of the Indonesian Deposit Insurance Corporation (LPS).

Important information on ESG and sustainable investing

Today we finance a number of industries that significantly contribute to greenhouse gas emissions. We have a strategy to help our customers to reduce their emissions and to reduce our own. For more information visit www.hsbc.com/sustainability.

In broad terms “ESG and sustainable investing” products include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors to varying degrees. Certain instruments we classify as sustainable may be in the process of changing to deliver sustainability outcomes. There is no guarantee that ESG and Sustainable investing products will produce returns similar to those which don’t consider these factors. ESG and Sustainable investing products may diverge from traditional market benchmarks. In addition, there is no standard definition of, or measurement criteria for, ESG and Sustainable investing or the impact of ESG and Sustainable investing products. ESG and Sustainable investing and related impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the ESG / sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of ESG / sustainability impact will be achieved. ESG and Sustainable investing is an evolving area and new regulations are being developed which will affect how investments can be categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.

THE CONTENTS OF THIS DOCUMENT OR VIDEO HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN HONG KONG OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT OR VIDEO. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT OR VIDEO, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

© Copyright 2026. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document or video may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.